Executive Summary

Agricultural commodities are entering 2025 with supply chains largely stabilized, global inventories at strong levels, and price pressures easing compared to the volatility of the early 2020s. Yet while the aggregate World Bank Agricultural Price Index is forecast to decline by 4.2% in 2025, disaggregated trends reveal a more complex, sector-specific landscape. Macroeconomic forces, including moderating global growth, shifting energy dynamics, climate volatility, and geopolitical uncertainties, will continue to shape agricultural markets. This article delivers a comprehensive, BCG-style analysis of the 2025 ag outlook, key sectoral trends, and critical risks for market participants.

Macro Backdrop: Decelerating Growth, Easing Inflation, and a Normalizing Commodity Cycle

Global macroeconomic conditions are stabilizing after a period of intense disruption. The International Monetary Fund projects global GDP growth at 2.7% in 2025, broadly in line with 2024 estimates but weaker compared to the pre-pandemic decade. Inflationary pressures have receded across most advanced and emerging economies, thanks to monetary tightening cycles and declining prices of energy and food commodities.

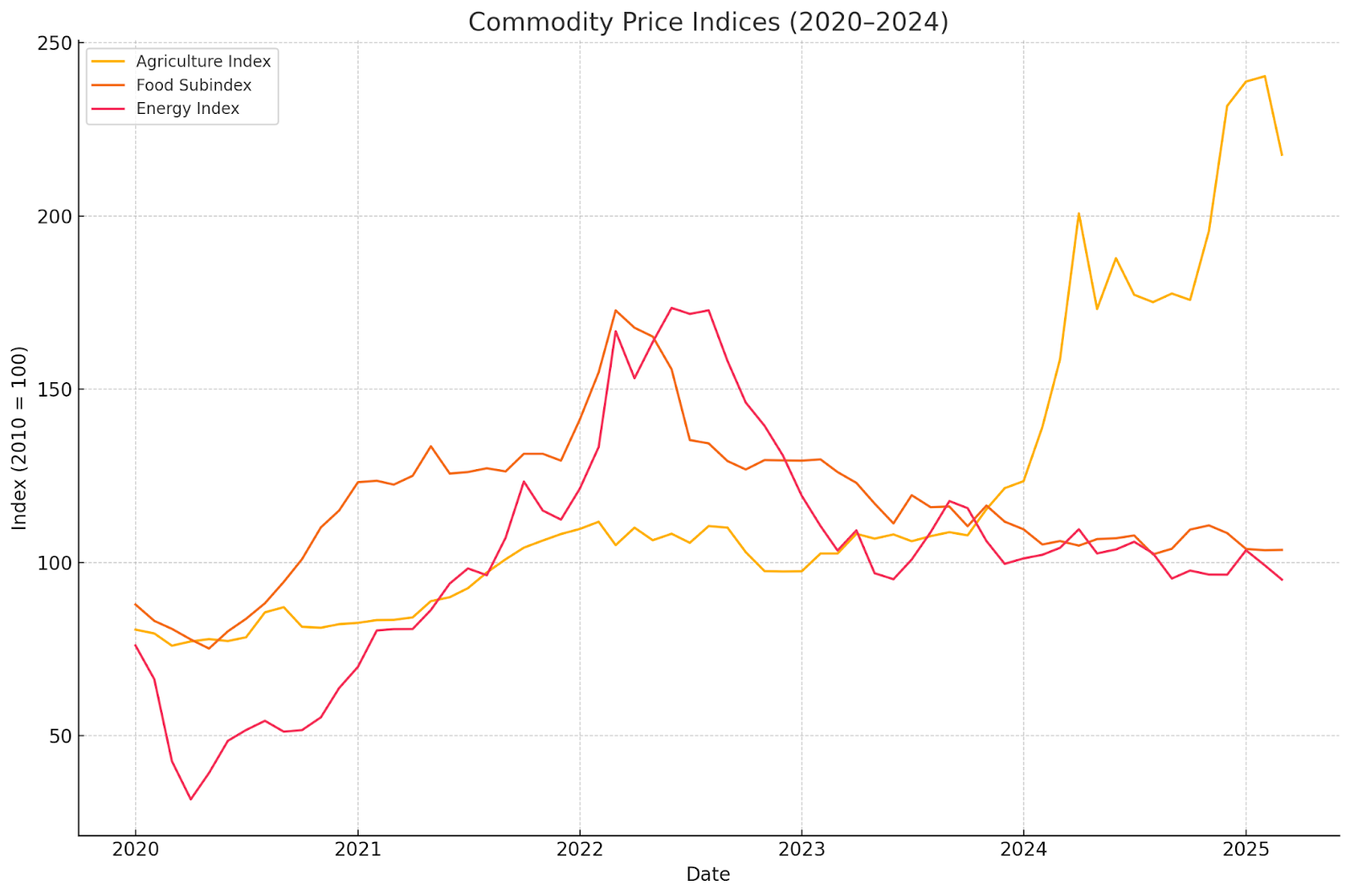

The World Bank’s October 2024 Commodity Markets Outlook highlights that after a 3% year-over-year softening in 2024, overall commodity prices are expected to retreat further by 5% in 2025. Agricultural commodities, in particular, reflect strong fundamentals, with most major crop categories recording large harvests and improving global inventories.

Despite this benign macro setting, the risk environment remains complex. Trade tensions, extreme weather events linked to climate change, and conflict-driven supply disruptions could rapidly alter market dynamics.

Fundamentals of the Agricultural Sector

Grains and Oilseeds: Oversupply Pressures Emerge

- Maize: Global maize output is projected to remain robust in 2025, following record harvests in the United States and Brazil. The International Grains Council estimates global maize production for 2024/25 at 1.22 billion metric tons, supported by favorable weather and high acreage. Maize prices are forecast to average $185/mt, a 1.1% decline from 2024 levels.

- Wheat: Despite localized droughts in parts of Canada and Australia, global wheat supplies remain ample. Recovery of Ukrainian wheat exports through Black Sea corridors and resilient production in Russia are key contributors. Wheat prices are expected to soften by 1.9%, averaging $265/mt.

- Soybeans: Oversupply pressures dominate the soybean complex. Brazil’s record harvest and expanded acreage in Argentina and the U.S. Midwest weigh on prices. Forecasts suggest a 5.5% year-over-year price decline, with soybeans averaging $430/mt in 2025.

Beverage Commodities: Weather-Driven Volatility Persists

- Cocoa: Cocoa markets experienced historic price surges in 2024 (+110%), driven by disease outbreaks, notably swollen shoot virus in West Africa, and adverse weather. Although a modest correction (-13% y/y) is projected for 2025, structural supply tightness and climate risks keep cocoa prices elevated relative to historical norms.

- Coffee: The prices of Arabica and Robusta coffee are forecast to decline by 7–9% as Brazil and Vietnam recover from weather-related disruptions. Nonetheless, continued vulnerability to climate variability, notably in Minas Gerais and the Central Highlands, necessitates caution.

Other Food Commodities: Regional Dynamics Key

- Rice: Global rice markets are forecast to soften by 11.4% in 2025, following sharp increases in 2024, driven by Indian export restrictions and the impact of El Niño on Asian harvests. Improved conditions in India, Thailand, and Vietnam underpin the outlook.

- Sugar: Sugar prices remain contingent on Brazilian production trends and Indian export policies. Stability is expected in 2025, though upside risks persist if weather impacts Brazilian cane yields.

Macro Drivers Shaping 2025 Agricultural Markets

1. Energy Price Trends and Agricultural Input Costs Lower global energy prices are easing production cost pressures. Brent crude oil is forecast to average $73/bbl in 2025, down 8.8% from 2024, while U.S. natural gas prices, critical for nitrogen fertilizer production, are expected to rise modestly (+54.5% y/y) as LNG export capacity expands. Fertilizer markets reflect easing conditions: prices for urea, DAP, and phosphate rock have retreated from post-pandemic highs, improving planting margins for major producers.

2. Climate Risk and Weather Volatility Although the current El Niño cycle is forecast to dissipate by mid-2025, residual weather anomalies remain a risk. The World Meteorological Organization confirmed 2024 as the hottest year on record, reinforcing the structural backdrop of climate-driven yield volatility. Drought risks in Southern Africa, South Asia, and parts of Australia merit particular attention, while potential flooding in Latin America could affect second-season soybean and maize crops.

3. Geopolitical and Trade Policy Risk Conflict remains a persistent tail risk. A renewed escalation in Middle East tensions could drive energy price spikes, which could then cascade into higher agricultural input costs. Furthermore, new rounds of trade restrictions, particularly in food security-sensitive crops like rice and wheat, could trigger localized price shocks and revive concerns about food inflation, especially in emerging markets.

4. Demand-Side Uncertainties: China and Emerging Markets China’s macro trajectory is central to oilseed and feed grain demand. While stimulus measures aim to stabilize economic growth, structural weaknesses in the property sector and declining consumer confidence could constrain imports. Conversely, steady growth in South Asia and Sub-Saharan Africa supports medium-term demand resilience for grains and edible oils.

Risk Scenarios and Strategic Implications

| Risk Factor | Scenario | Impact on Agricultural Commodities |

| Conflict Escalation | Middle East conflict disrupts oil flows, energy prices spike | Higher fertilizer and transportation costs; upward pressure on grains, edible oils |

| Extreme Weather Events | Droughts in the U.S., Brazil, or Australia; floods in Asia | Localized supply shocks; volatility in maize, soybean, and rice markets |

| Trade Restrictions | Major exporters impose bans (e.g., India for rice, Russia for wheat) | Price surges in affected commodities; renewed food security concerns |

| China Growth Shocks | Weaker-than-expected Chinese industrial activity and imports | Demand softness for oilseeds and feed grains, potential price weakness |

Strategic Outlook for 2025

Traders and market participants should position for generally softer baseline prices in grains and oilseeds, but remain tactically agile due to elevated weather, geopolitical, and demand-side risks. Key strategies include:

- Weather risk hedging is significant for grains and tropical commodities.

- Monitoring fertilizer input costs: Fertilizer affordability remains a margin-sensitive variable for crop production trends.

- Vigilance on trade policy shifts: Rapid adjustments to export policies can create asymmetric risks.

- Scenario planning around China: Sensitivity of oilseed markets to Chinese import behavior requires dynamic modeling.

Flexibility, disciplined positioning, and a differentiated approach across agricultural subsectors will be crucial to navigating the 2025 landscape.

Disclaimer: This communication is intended for informational purposes only and does not constitute trading advice. Futures and options trading involve substantial risk of loss and are not suitable for all investors.